Loan balance still meaningful

Switching tends to matter more when the loan size is still significant.

A practical comparison of HDB concessionary loans and bank home loans — including interest rates, flexibility, and when switching to a bank loan may make sense.

Last updated: March 2026

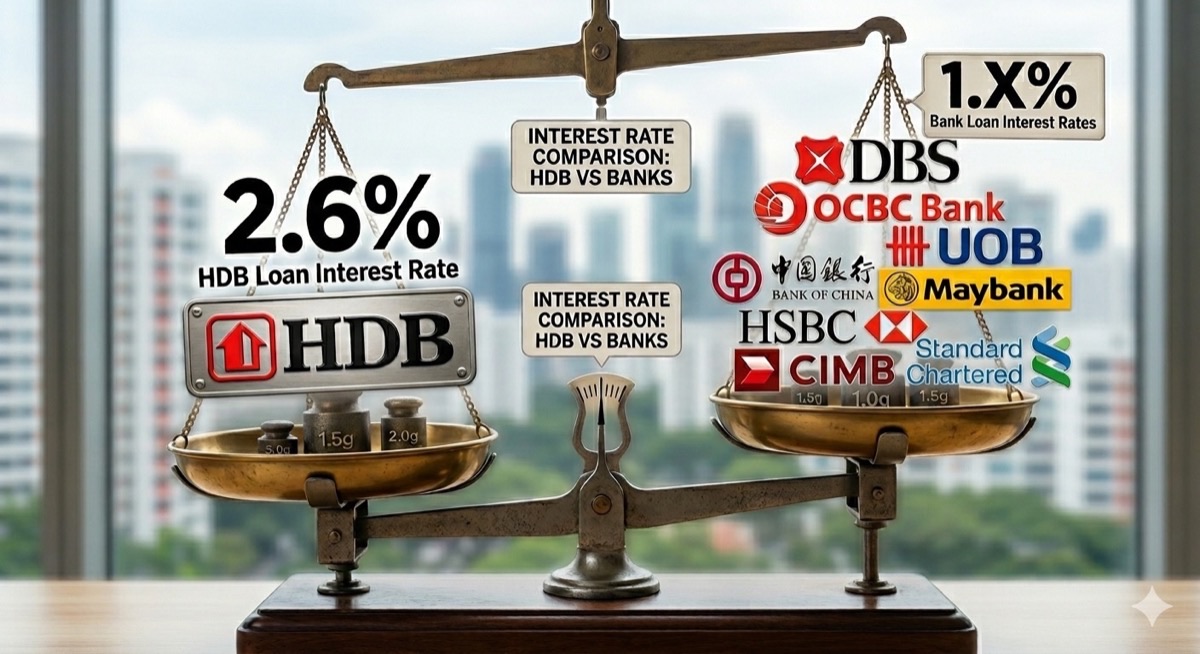

HDB concessionary loans have a stable interest rate, but bank home loans have historically been cheaper over the long term.

Many HDB owners eventually refinance from HDB loans to bank loans once their loan balance and financial situation allow it.

Switching is often considered when:

| Feature | HDB Concessionary Loan | Bank Home Loan |

|---|---|---|

| Interest Rate | Fixed at CPF OA rate + 0.1% | Market-based |

| Current reference | Usually 2.6% | Varies by package |

| Rate changes | Rare | Changes with market |

| Flexibility | Very flexible repayment | Depends on package |

| Early repayment | No penalty | Lock-in may apply |

The HDB concessionary rate is pegged to the CPF Ordinary Account rate.

Because the CPF OA rate is currently 2.5%, the HDB loan rate has been 2.6% for many years.

Even though bank rates rose during the global interest rate cycle between 2022 and early 2025, historically bank home loan rates have often been lower than the HDB concessionary rate of 2.6%.

For long-term homeowners, this difference can lead to meaningful savings over time.

Borrowers should evaluate long-term cost rather than focusing only on short-term rate movements.

Switching tends to matter more when the loan size is still significant.

Even a 0.4%-0.8% difference can create meaningful annual savings.

Stable income and credit profile help qualify for bank packages.

Bank loans may offer more competitive pricing over time.

In many cases, switching to a bank loan becomes practical once the remaining loan balance is around S$250,000 or more.

At this level:

Borrowers should still compare package terms carefully because legal costs, lock-in clauses, and rate structure differ between banks.

Loan balance: S$400,000

Rate difference: 0.6%

Annual interest difference:

S$400,000 x 0.6% = S$2,400 per year

Over several years, even modest rate differences can accumulate into noticeable savings.

Actual savings depend on amortisation schedule and package clauses.

HDB loans allow partial repayment without penalty.

Savings from switching may be minimal.

HDB loan rate changes very rarely.

Ask yourself:

We can review your current loan and estimate whether refinancing could reduce your interest cost.

Not always. HDB loan rate is stable at CPF OA + 0.1%, but bank rates have historically often been lower over long periods.

Yes. Many homeowners refinance from HDB loans to bank loans once they qualify for bank financing.

Switching often becomes practical when the remaining loan balance is around S$250,000 or higher, although each case differs.

HDB itself does not charge a penalty, but the new bank loan may have its own lock-in structure.