End of lock-in period

This is the most common refinance timing because penalties may no longer apply.

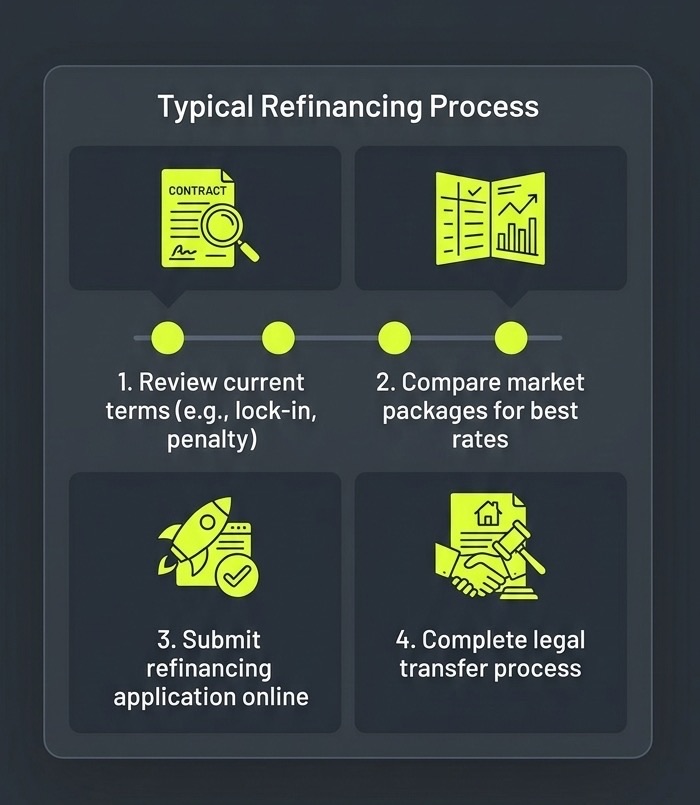

Refinancing can reduce your mortgage cost, but the right time depends on lock-in terms, legal costs, cash rebates, flexibility to prepay during lock in, flexibility to sell during lock in, or how soon you can convert the rates while in the lock in and how long you plan to keep the property.

Last updated: March 2026

What this page helps you do: decide whether switching banks is worth the cost and effort, or whether repricing or waiting is the better move.

Percent operates under FindAHomeLoan Pte Ltd (established 2014), supporting refinancing reviews across major local and foreign banks in Singapore.

Refinancing usually makes sense when your current package is no longer competitive and the expected savings are larger than the switching costs.

The decision should not be based on headline rate alone.

You should compare:

This is the most common refinance timing because penalties may no longer apply.

If your package has rolled to a higher reversion rate, refinancing may reduce monthly cost.

The more years you expect to keep the property, the more time you have to recover switching costs.

Refinancing tends to matter more when the outstanding balance is still large enough for rate changes to create visible savings.

Penalties and clawback can outweigh near-term savings.

A short holding period reduces the value of switching.

Rate savings may be too small to matter.

Sometimes staying with the same bank is simpler and good enough.

| Feature | Repricing | Refinancing |

|---|---|---|

| Stay with same bank | Yes | No |

| Legal work | Usually less | Usually more |

| Package choice | Limited to existing bank | Wider market choice |

| Admin effort | Lower | Higher |

| Best when | Current bank offers fair terms | Better market rates exist elsewhere |

Repricing may be simpler, but refinancing may offer wider package choice and stronger long-term savings.

Loan balance: S$800,000

Current rate: 2.5%

New rate: 1.5%

Estimated difference: about 1.0%

Approximate annual interest saving:

S$800,000 x 1.0% = S$8,000 per year

This is only a simple illustration. Actual savings depend on amortisation, fees, lock-in terms, legal subsidies, and how long you keep the new package.

| Cost / Clause | Why it matters |

|---|---|

| Lock-in penalty | Can cancel out savings if you refinance too early |

| Cash rebate clawback | Some subsidies may need to be repaid |

| Legal fees | Switching banks often involves legal work |

| Valuation fee | Some refinance cases require fresh valuation |

| Notice period | Timing matters if you want a smooth switch |

Ask yourself:

We can compare your current package against market options and explain the real cost difference, not just the headline rate.

Refinancing usually makes sense when your current package is no longer competitive and the expected savings are larger than switching costs. Borrowers should compare lock-in penalties, clawback, legal fees, valuation cost, and expected holding period before switching.

Repricing may be simpler because you stay with the same bank and usually face less legal work. Refinancing can offer a wider package choice and stronger savings if better market rates exist elsewhere.

Savings depend on the gap between your current rate and the new package, your outstanding balance, fees, subsidies, and how long you keep the property. A simple example is an S$800,000 loan with a 1.0% rate difference, which may imply roughly S$8,000 in annual interest difference before fees.

Borrowers should check lock-in penalties, cash rebate clawback, legal fees, valuation fees, and notice periods before switching. These items can materially change whether refinancing is worthwhile.